Strategic Straits & Vulnerable Europe

Europe's Energy Supply After the Russian Shock: Are Strategic Maritime Passages the New Achilles' Heel?

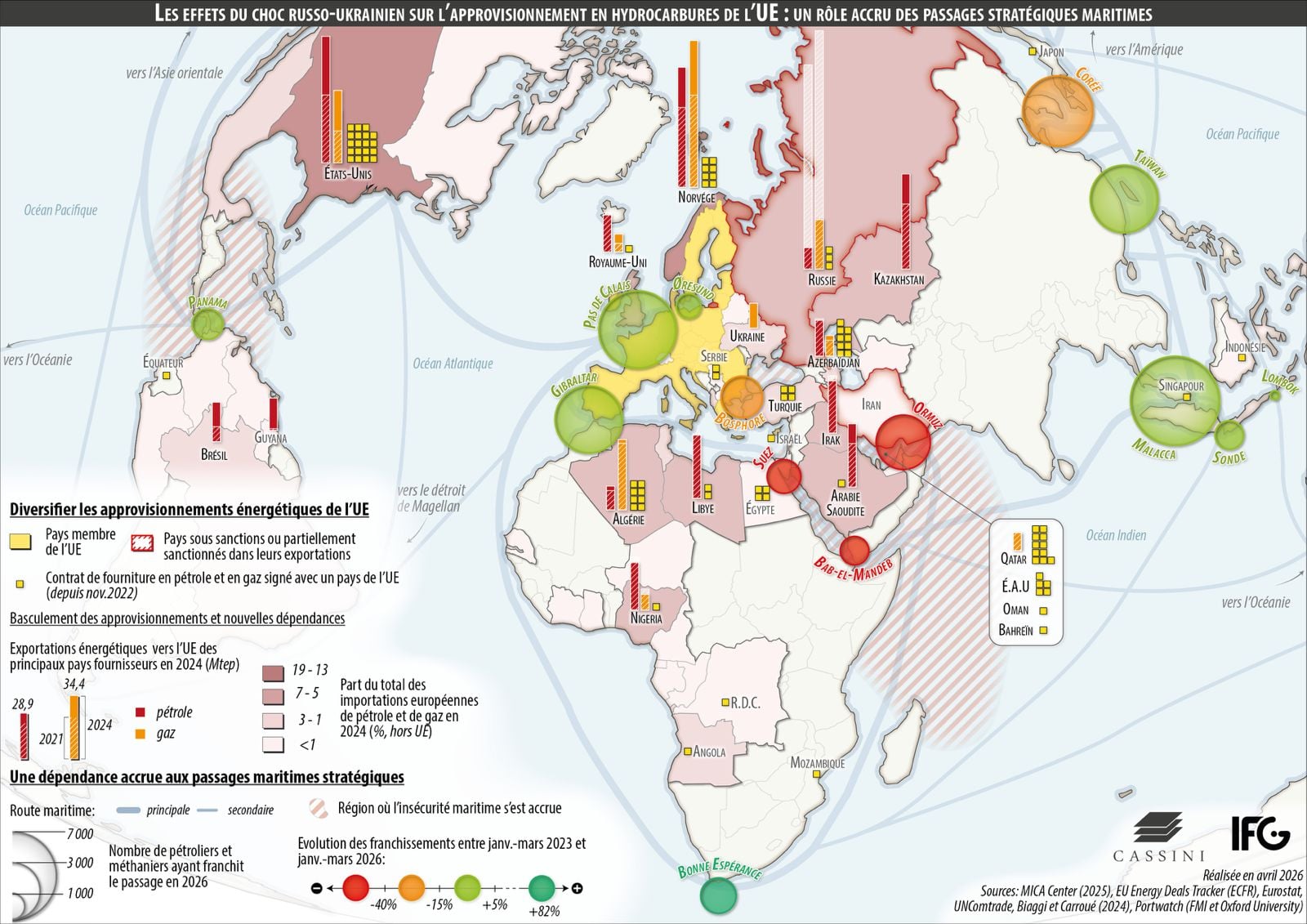

Towards a Structural Vulnerability of European Energy Supply to Navigability Conditions in Strategic Maritime Passages?

Since 1 March, Iran's blockade of the Strait of Hormuz — the result of escalating conflict with the United States and Israel — has highlighted the strategic importance of maritime passages for the global circulation of hydrocarbon flows. Yet stepping back from current events and mapping the evolution of European energy supply over recent years reveals that Europe is today more vulnerable than before to disruptions in maritime traffic along these navigation corridors.

Europe's Post-2022 Oil and Gas Diversification Strategy

In the aftermath of Russia's invasion of Ukraine, European states' dependence on imports of Russian oil and natural gas became a vulnerability for the security of the European Union. In addition to imposing a series of economic sanctions, the EU adopted an ambitious strategy, known as REPowerEU, aimed at completely phasing out Russian hydrocarbons by 2027. The plan rests on a diversification of gas and oil suppliers. It has taken shape through the signing of 88 new supply contracts (yellow squares), primarily for gas, with around twenty different countries, led by the United States, Qatar, Norway, Azerbaijan, and Algeria.

A Growing Maritimisation of Hydrocarbon Flows Towards Europe

Two years on, the effects of this policy are already being felt. In 2024, Russian oil and gas exports to Europe reached a historic low, offset by increased flows from major producing countries such as Norway, the United States, Saudi Arabia, and Kazakhstan, as well as new suppliers including Brazil and Guyana (bar chart). As a result, Europe's energy landscape has rebalanced (colour shading): Russia now accounts for only 5% of the EU's external hydrocarbon supply, far behind Norway (19%) and the United States (13%).

Whereas previously a significant share of the oil and gas consumed in Europe was transported by pipeline from Russia, these supplies now travel more frequently by sea, along the major global trade routes, from ever more distant states. This maritimisation of flows is particularly pronounced for gas, whose market is less globalised than that of oil and has long relied heavily on maritime transport. While liquefied natural gas accounted for only 16% of EU gas imports in 2021, it now represents approximately 40% of total imports in 2023 and 2024.

Heightened Vulnerability to Disruptions in Maritime Passages

These maritime routes have an Achilles' heel: a handful of chokepoints that shape their trajectories. Several of these straits, canals, and capes are essential to the global circulation of hydrocarbon flows (proportional circles). In the first three months of 2023, nearly 24,000 tankers and LNG carriers crossed the straits of Malacca, Dover, Korea, and Hormuz. Due to the geographical characteristics of these passages, the fluidity of traffic is exposed to a range of logistical, climatic, and security risks.

The resurgence of tensions in the Middle East since the Hamas attack on Israel on 7 October 2023 has severely degraded navigability conditions in the region's maritime passages, where the number of crossings was halved between January and March 2026 compared to the same period in 2023. For nearly two years, Yemeni Houthi attacks on vessels in the Red Sea, combined with a resurgence of piracy off the Horn of Africa, have led shipowners to reroute around the Cape of Good Hope, adding 10 to 15 days to journeys. The situation in the Persian Gulf is more concerning: with no real alternative exit beyond the Strait of Hormuz, vessels are forced to wait for the passage to be reopened by the belligerents.

For the time being, the effects of this crisis on European supply remain limited, as the countries of the region account for only a modest share of the EU's oil and gas imports. Nevertheless, the uncertain outcome of the conflict, together with the destruction affecting energy infrastructure in the Gulf, is undermining Europe's diversification strategy. Indeed, the states of the region — Qatar foremost among them — have concluded around twenty new gas and oil supply contracts with the European Union, contracts intended to help Europe achieve its energy independence objectives with respect to Russia.