The Rise of FakeInfra

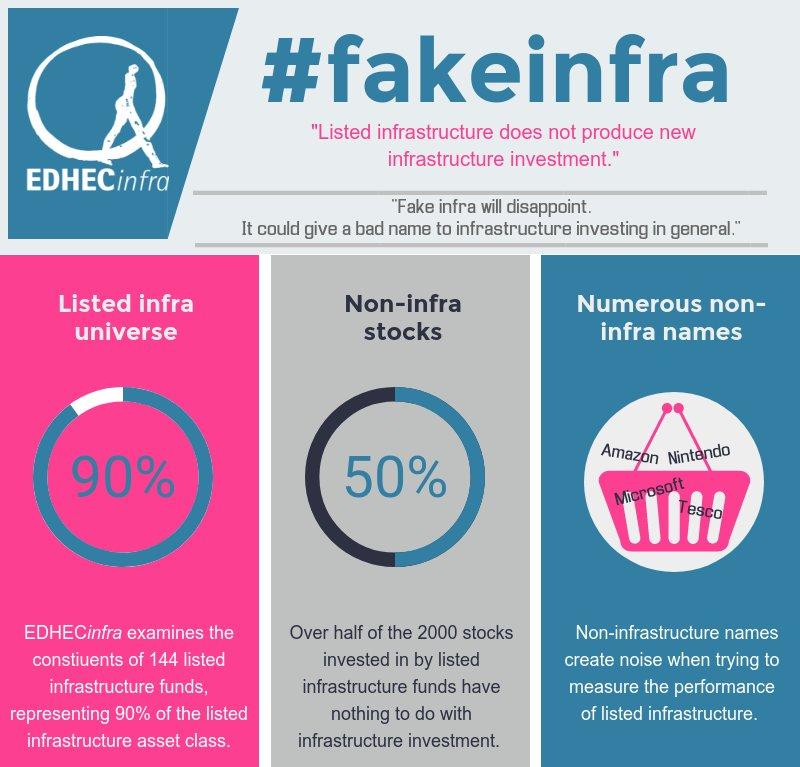

EDHECinfra, an EDHEC singaporean academic research organization for infrastructure investment performance, has revealed “the rise of fake infra” in a recent study : “Half of the stocks in listed infrastructure funds have nothing to do with infrastructure investments.”

The video below is explaining the main findings of the EDHECInfra paper:

Find out More:

► Read "Fake Infra" written by Sarah Tame in the Finance section of EDHECVox, Associate Director and Chief communications officer at EDHEC Infrastructure Institute, EDHEC Business School

► Read the full study entitled "The Rise of Fake Infra" co-authored by Noël Amenc, Professor of Finance, EDHEC Business School Associate Dean, CEO of Scientific Beta, Frédéric Blanc-Brude, Director, EDHEC Infrastructure Institute, Aurélie Chreng, Senior Research Engineer, EDHEC Infrastructure Institute and Christy Tran, Senior Data Analyst, EDHEC Infrastructure Institute