How to improve the risk management of pension funds?

We are pleased to enclose recent research on retirement solutions and safe retirement income entitled “Improving Interest Rate Risk Hedging Strategies through Regularization, by Daniel Mantilla-Garcia, Lionel Martellini, Vincent Milhau, and Hector Enrique Ramirez, published in the Financial Analysts Journal, a CFA Institute publication.

Daniel Mantilla-Garcia, EDHEC PhD (2012), Research Associate, EDHEC-Risk Institute, Assistant Professor of Finance, Universidad de Los Andes

Lionel Martellini, Professor of Finance, EDHEC Business School, Director, EDHEC-Risk Institute

Vincent Milhau, Research Director, EDHEC-Risk Institute

Hector Enrique Ramirez-Garrido, Research Assistant, Universidad de Los Andes

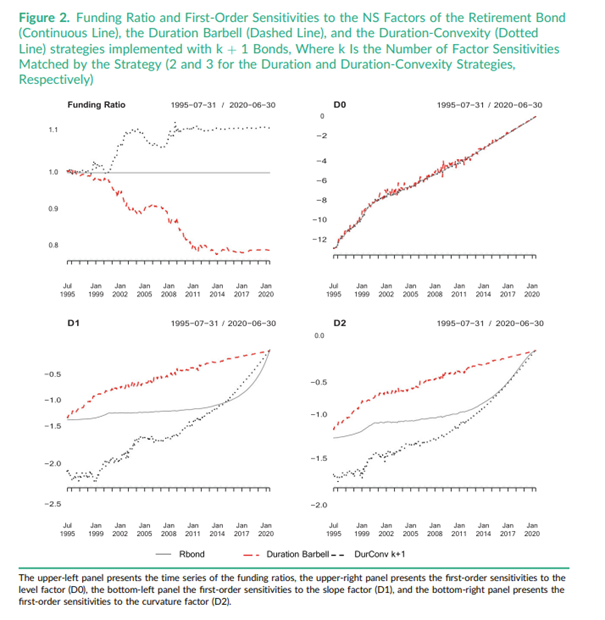

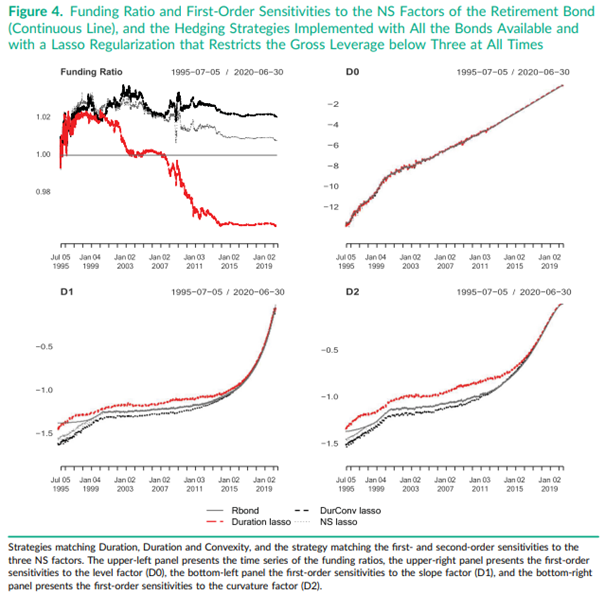

The effectiveness of duration and convexity hedging strategies deteriorates in the presence of non-parallel shifts of the yield curve. In the absence of appropriate constraints, the extension of these strategies accounting for changes in the shape of the yield curve generates unstable weights and extreme leverage, leading to poor out-of-sample hedging performance.

To address this conundrum, authors recast the bond portfolio immunization problem as a multifactor optimization program with leverage constraints and weight regularization. These regularized immunization strategies offer a robust improvement in hedging performance and are particularly well-suited to secure future cash flow needs such as pension liabilities.

“An important application of what we do in the paper, is to better manage the risk of pension funds, particularly, to construct more robust pension liability hedging portfolios” says Daniel Mantilla, EDHEC-Risk Institute Associate Researcher and PhD, EDHEC Business School.

KEY FINDINGS

- Hedging against non-parallel shifts in the yield curve is of major practical importance for institutions like pension funds or insurance companies endowed with long-term liabilities

- We use machine learning techniques to build more robust hedging strategies that protect investors against general shifts in the yield curve

- The proposed immunization strategies offer a substantial improvement in hedging performance and a strong reduction in leverage and turnover compared to the standard unconstrained approach to bond portfolio immunization

The article is in open access at the following link: doi.org/10.1080/0015198X.2022.2095193.

#interestratehedging #pensionliabilityhedging #robustbondportfolioimmunization