THE IMPACT OF MARKET CONDITIONS ON BOND FUND MANAGERS

Editorial written by Dr Harsh Parikh,

EDHEC PhD in Finance graduate (2016), Principal, PGIM Institutional Advisory & Solutions, USA.

The Impact of Market Conditions on Bond Fund Managers

Most of the academic literature investigating active management finds that active managers in aggregate underperform relative to their benchmarks. Overall and for subcategories of bond funds, Blake, Elton, and Gruber [2010] show that fund managers underperform relevant indexes after expenses are taken into consideration. Fischer and Wermers [2012, p. 287], however, note that the proponents of active management argue its benefits are most pronounced in periods of heightened volatility and economic stress. Support for this claim is provided by Kacperczyk, Nieuwerburgh, and Veldkamp [2013] who show that the effectiveness of manager skills is not only time-varying but also market-environment-dependent. Reibnitz [2015] shows active equity strategies have the greatest impact on returns during periods of high dispersion, when alpha produced by the most active funds significantly exceeds that produced in other months. The active management literature cited above focused principally on equity markets. In this paper, we validate whether these findings hold in the case of active fixed income management.

Data and Methodology

In order to define opportunity in the fixed income space, for our study we use (1) the Merrill Option Volatility Estimate (MOVE), a bond-implied volatility measure similar to VIX for stocks, and (2) cross-sectional volatility, the standard deviation of fixed income sector returns (CSV), as a measure of dispersion. We use eVestment U.S. core plus fixed income universe for manager performance, gross of fees, to address these research questions. For a benchmark proxy we use an equal weighted fixed income sector benchmark; this choice of using average performance aligns with using CSV as a dispersion indicator. In order to evaluate the impact of opportunity on outperformance, we used a monthly vector autoregressive model of order 1, VAR(1). The model allows us to understand the interdependencies of these three endogenous variables: implied volatility (MOVE), cross-sectional volatility in fixed income sector returns (CSV), and the 25th percentile manager outperformance (TOPA). We account for the style biases since our dependent variable is manager outperformance, as measured by manager returns in excess of benchmark returns. Change in the U.S. 10-year government yield, denoted by D(YIELD), is the exogenous variable in the model.

Several robustness checks are also reported to ensure the validity of our findings by similarly assessing the volatility impact on equity manager outperformance and by conducting extensive factor analysis on fixed income manager outperformance (using principal component factors). For brevity, we do not report them here.

We propose a timing strategy between active and passive. For the portfolio formation at time t, we allocate to an active strategy for three months when the average cross-sectional volatility for the last three months is greater by one half of a standard deviation than the long-term average.

Empirical Results

In our paper, we review manager outperformance conditional on interest rate regimes and conditional on changes in volatility. In providing this review we show that the opportunity and effectiveness of manager skills are time-varying (not reported here).

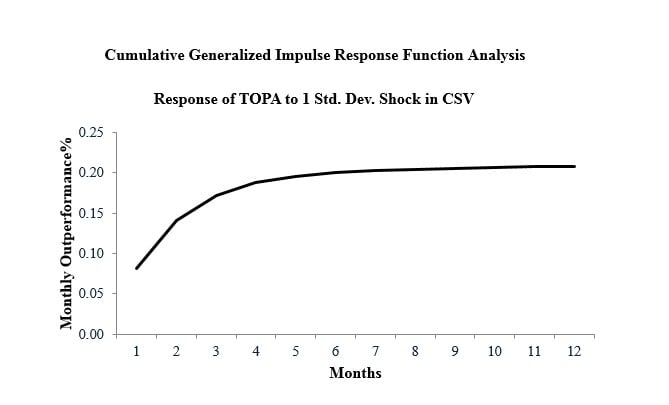

Using the VAR(1) model, we empirically establish and quantify the relationship of manager outperformance with dispersion (cross-sectional volatility) and volatility (time series). The contemporaneous relationship of D(YIELD) to the 25th percentile manager outperformance (TOPA) denotes that for every 100 bps change in yield, TOPA rises by 115 bps. In addition to benefitting from changes in yields, our analysis shows that there is persistent outperformance added from increases in cross-sectional volatility (see Figure). The generalised impulse response of the 25th percentile manager outperformance to a one standard deviation shock to cross-sectional volatility in fixed income sector returns accumulates to 21 bps over 12 months. To illustrate, mean TOPA is 26 bps in the sample, i.e., TOPA would increase by almost 80% with the shock in CSV.

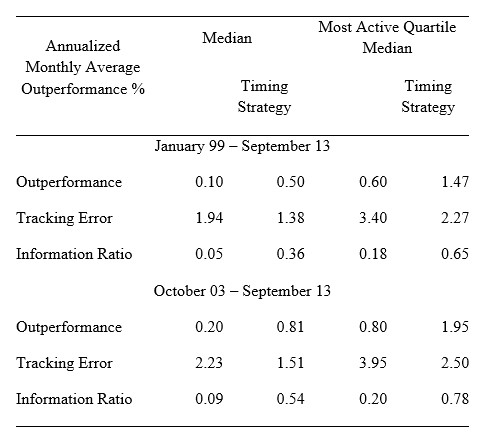

We show, using cross-sectional volatility in spread sectors as an indicator, an effective timing strategy to time between active and passive. The results of the table show that the Information Ratio (IR) of the timing strategy with the most active[1] median manager improved from 0.18 to 0.65. For the timing strategy with median manager, the IR improved from 0.05 to 0.36. Throughout the evaluation period, the strategy is active 40% of the time and passive 60% of the time.

Timing Strategy Using Spread Sector Based Indicator

This exhibit shows annualised monthly average for both median and most active quartile median outperformance with and without employing aforementioned timing strategy. Timing is based on cross-sectional volatility in spread sectors.

There is persistent outperformance added from increases in cross-sectional volatility. Moreover, investors can also benefit from persistence of dispersion by scaling the active risk budget.

Conclusion

Rising interest rate environments tend to be associated with uncertainty in bond yield; for example, higher implied volatilities and increased cross-sectional dispersion of returns across sectors. Our analysis shows that active managers have relatively shorter duration and longer spread duration exposure, thereby benefitting from rising rates. We also attribute outperformance to the increased cross-sectional volatility, since it presents larger than normal opportunities, and skilled managers can capitalise on these opportunities. We also find increased outperformance as measured by the information ratio for most active managers, particularly during times of increased uncertainty and dispersion. As illustrated with timing strategies, investors can also benefit from persistence of dispersion by scaling the active risk budget.

References

Blake, C. R., E.J. Elton, and M.J. Gruber. 2010. “Performance of Bond Mutual Funds.” Journal of Business, Vol. 66, No. 3, pp. 371-403.

Fischer, B., and R. Wermers. 2012. Performance Evaluation and Attribution of Security Portfolios. Oxford: Academic Press.

Kacperczyk, M., S. Nieuwerburgh, and L. Veldkamp. 2014. “Time-Varying Fund Manager Skill.” Journal of Finance, Vol. 69, No. 4, pp.1455-1484.

Reibnitz, A. 2015. “When Opportunity Knocks: Cross-Sectional Return Dispersion and Active Fund Performance.” Working Paper.

This editorial is based on the article published in the Journal of Fixed Income (Winter 2018, 27 (3) 6-22) co-authored with Professor Frank Fabozzi. Harsh Parikh, PhD (2016), one of the authors, successfully defended his thesis “Two essays in Empirical Finance” in August 2016 at the London campus. Thesis committee: Professors Serge Darolles (Université Paris-Dauphine), Lionel Martellini and Rene Garcia (EDHEC Business School). This research paper represents the views and opinions of Harsh Parikh and not necessarily the views of PGIM, Inc. or any of its subsidiaries or affiliates. This paper is for educational purposes only and is not intended to be used as investment advice or recommendation by person or persons in possession of this material.

[1] Activeness is measured by the in-sample ex-post tracking error of the manager.