Still Too Big to Fail?

EDHEC PhD in Finance Newsletter - June 2020

Editorial © signed by Darrell Duffie[1] , Adams Distinguished Professor of Management and Professor of Finance at the Graduate School of Business, Stanford University

Still Too Big to Fail?

Before the failure of Lehman Brothers in 2008, it was generally assumed that systemically important financial institutions (SIFIs) were too big to fail.That is, if a huge bank were to approach insolvency, the government would be almost forced to bail out the bank. The alternative would be to allow the bank to fail, causing catastrophic damage to the economy. In effect, the economy was held hostage, with the situation demanding a ransom of government capital to nationalize the bank and stabilize the economy. During the Great Financial Crisis of 2008-2009, bailouts were frequent, in multiple countries. For example, by investing 46 billion pounds of public money, the U.K government rescued the Royal Bank of Scotland from insolvency.

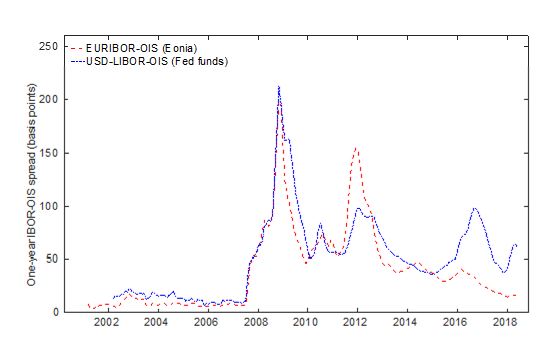

Although bailouts generally wiped out the shareholders of the rescued banks, the creditors were made whole. Before the crisis, the presumption of too-big-to-fail bailout support led creditors to lend money to giant banks at razor-thin credit spreads, on average around only 10 basis points for one-year funding, as shown in Figure 1, despite the extreme leverage of the largest banks.

However, Lehman Brothers was not bailed out. Moreover, through legislation and the post-crisis Basel regulatory process, essentially all developed-market governments developed methods by which the creditors of large banks would no longer need to get paid in full to avoid a disaster when a large bank neared insolvency. Instead, in a new process called “bail-in,” creditors would be forced to fund the recapitalization of a failing large bank by having a substantial fraction of their debt claims substituted with equity shares, returning the bank to a safe degree of leverage. Although bail-in has yet to be attempted for an extremely large bank, bank creditors appear to have taken to heart the U.S. government’s decision not to bail out Lehman and the post-crisis development of bail-in. Post-crisis credit spreads never returned to pre-crisis lows, as shown in Figure 1, despite substantial improvements in capitalization (again through the Basel process).

Figure 1. The spread between one-year US dollar LIBOR and the one-year overnight index swap rate, a proxy for risk-free one-year yields.

In research with Antje Berndt and Yichao Zhu, we find that the credit spreads of systemically important U.S. banks roughly doubled at a given leverage, controlling for time variation in corporate-debt default risk premia. Using a combination of a nonlinear panel regression of credit spreads and a structural asset-pricing model of the relationship between credit spreads, equity prices, and balance sheet data, we also estimate substantial reductions in the “risk-neutral” probability of bailout. For example, the data are consistent with a reduction in the risk-neutral bailout probability (given insolvency) of globally systemically important U.S. banks (GSIBs) from 0.65 before Lehman failed to approximately 0.2 in the post-Lehman decade. This represents a significant reduction in effective government debt funding-cost subsidies, which we find accounted for about 31% of the pre-crisis equity market value of U.S. GSIBs.

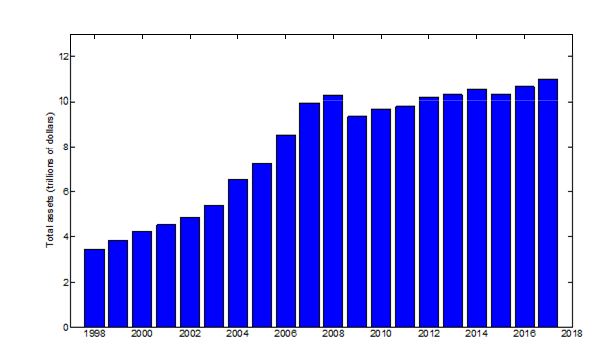

The reduction in debt subsidies for GSIBs dramatically reduced the appetite for these banks to expand their balance sheets, as shown in Figure 2. No longer does the prospect of a bailout cause GSIBs to grow their balance sheets rapidly, fueled by subsidized funding costs, as explained in Andersen, Duffie, and Song (2019).

It remains, however, to see whether governments will have the resolve to actually deploy their bail-in methodologies the next time that a systemically important bank approaches failure. That is the next challenge.

Figure 2. The total assets of the holding companies of Goldman Sachs Group, Morgan Stanley, Merrill Lynch, Lehman Brothers, Bear Stearns, Bank of America, JP Morgan Chase, Citigroup, and Wells Fargo, from 10K disclosures.

[1] This note is based on the results of "The Decline of Too Big to Fail," with Antje Berndt and Yichao Zhu, Working paper, Australia National University, February, 2020.

References

Andersen, Leif, Darrell Duffie, and Yang Song. 2019. "Funding Value Adjustments," Journal of Finance, Volume 74, pp. 145-192.

Berndt, Antje, Darrell Duffie, and Yichao Zhu. 2020. "The Decline of Too Big to Fail," Working paper, Australia National University, December, 2019.

About the author:

Darrell Duffie is the Adams Distinguished Professor of Management and Professor of Finance at Stanford University’s Graduate School of Business. He is a Fellow and member of the Council of the Econometric Society, a Research Fellow of the National Bureau of Economic Research, a Fellow of the American Academy of Arts and Sciences. Duffie was the 2009 president of the American Finance Association. In 2014, he chaired the Market Participants Group, charged by the Financial Stability Board with recommending reforms to Libor, Euribor, and other interest rate benchmarks. Duffie’s recent books include How Big Banks Fail (Princeton University Press, 2010), Measuring Corporate Default Risk (Oxford University Press, 2011), and Dark Markets (Princeton University Press, 2012).

Darrell Duffie’s research interests include over-the-counter markets, banking, financial stability, credit risk, valuation and hedging of derivative securities, financial market infrastructure, the term structure of interest rates, financial innovation, security design, and market design.