Which one moves first: a study of long-term equilibrium and price discovery between Variance Premium, Credit Risk Premium and Bond Liquidity Premium

Special Issue - EDHEC PhD in Finance Newsletter - June 2020

Article signed by Jean-Paul Brasier, EDHEC PhD candidate, Head of Market Risk, Segantii, Hong Kong

Which one moves first: a study of long-term equilibrium and price discovery between Variance Premium, Credit Risk Premium and Bond Liquidity Premium

Since the seminal article by Merton (1974), numerous studies have been devoted to the structural modeling of corporate bonds as options on the underlying company. Empirical literature has shown that structural models of credit risk are poor predictors of credit spread levels, and, more particularly. that observed credit spreads are higher than those predicted by structural models. Subsequently, a substantial body of literature has focused on relationships between a firm’s credit spread premium and underlying equity volatility. In a 2001 paper, by studying the returns of delta-hedged equity options portfolios Bakshi and Kapadia showed evidence of a systematically positive variance premium: option implied volatility is almost always higher than expected realized volatility.

Wang, Zhou, and Zhou (2013) show that the credit spread puzzle and the variance premium puzzle are closely linked. Firm-level variance premium, measured as the difference between squared implied volatility and realized volatility, has a strong explanatory power for credit spreads. The predictive power of variance premium is higher than the simple implied variance derived from option prices. Another conclusion is that volatility increases the probability of default and therefore the credit spreads, a conclusion consistent with the predictions of classical asset pricing theory as envisaged in the framework of Merton (1974). However, Wang Zhou Zhou (2013) study is conducted over long time horizons – one to three months - and does not address issues faced by market practitioners focused on price discovery relationships and information flows at a daily horizon between equity option market and credit market.

Model set-up

To assess the existence of a long term equilibrium relationship between equity-variance premium, credit-risk premium and liquidity premium, to understand the relative speed at which different markets incorporate innovations and which market has the leading role, we use the framework of Vector Error Correction Model in a daily setting. VECM is a suitable model to investigate these types of dynamics. Longstaff et al. (2003), Norden Weber (2009), Forte Pena (2009) have implemented VECM in order to investigate existence of long-term equilibrium and pricing discovery between credit spreads derived from cash bonds, Credit Default Swaps (CDS) and the stock market. These authors generally conclude to the leading role of the stock market over CDS and the leading role of CDS over cash bonds. We supplement analysis of cointegration between our 3 variables by a composite pricing discovery measure using the Hasbrouq information share (IS) and Gonzalo Granger Composition Share (CS)[1].

Variables construction

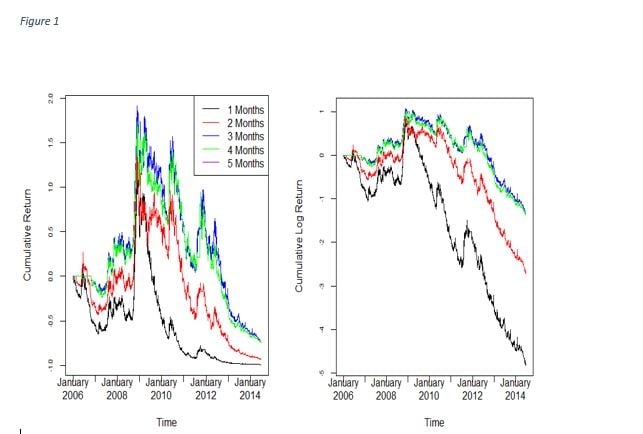

In Wang Zhou Zhu (2012), variance premium is not an investible asset and is not observable on a daily basis. Following Eraker and Wu (2014) and Travis Johnson (2017), we derive an investible and observable daily version of variance-risk premium from the return of a dynamic investment strategy in variance-sensitive assets: VIX futures of different maturities. Figure 1 presents the cumulative returns of our Vix future strategy.

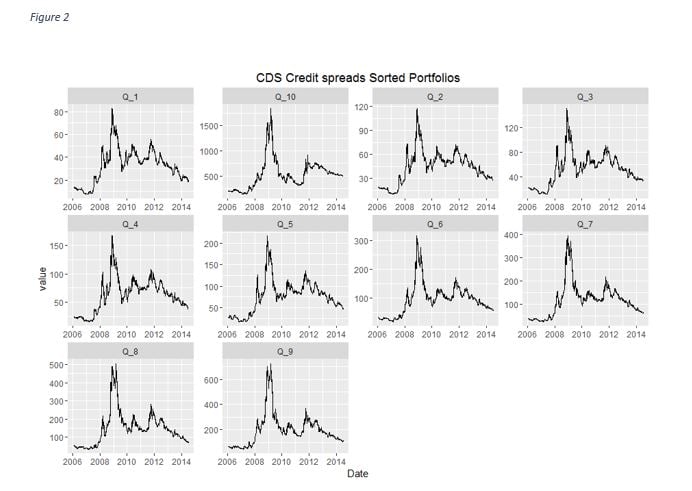

To model the credit-risk premium we use CDS spreads since the credit derivatives market, the place where credit is explicitly traded, is expected to provide a “pure” measure of credit risk. To understand the relationships between the equity-variance premium and different credit spread profiles, we relate to the concept of style portfolios developed in the equity anomaly pricing literature. We create Credit spread sorted and Industry sorted CDS portfolios. Credit spread sorted portfolios relate directly to the concept of credit carry strategy as defined by Brooks Palhares and Richardson (2018). Our credit-spread sorted and industry CDS portfolios built from daily observations of 169 corporate CDS on US companies, members of the S&P 500, with sufficient data between 2006 and 2014. Figure 2 presents the evolution of our Credit-Spread sorted CDS portfolios. The aggregate cash bond market liquidity variable is the Liquidity Cost Spread (LCS) published on subscription basis by Barclays Capital. LCS data are available since February 2007.

Derivation of a pair trading strategy

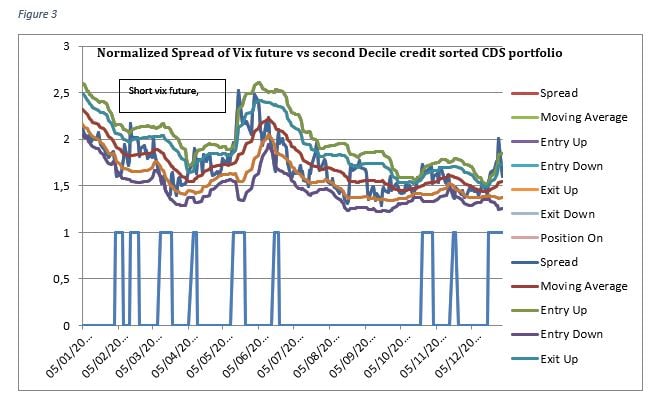

The framework of VECM and associated concept of long-run equilibrium is the workhorse of the pair-trading literature. Following Gatev, Goetzman and Rouwenhorst (2006) and Figuerola-Ferreti and Parskevopoulos (2012), we study the returns of pair-trading strategies between our VIX futures portfolios and credit-spread sorted and industry sorted CDS portfolios. Consistent profits from pair-trading strategies only exist if perturbations are transitory and adjustment towards equilibrium is not immediate. Following established practice, we base our trading rules on an historical standard deviation metric, we open a long–short position when the pair prices have diverged by a certain amount and close the position when the prices have reverted. An example of the implementation details of our pair-trading strategy is presented in figure 3.

Our main findings

Under linear VECM specification, all 3-tuple (Variance premium, Credit, Liquidity) and 2-tuple (Variance premium, Credit) and (Credit Liquidity), where Credit variable refers to Credit sorted and industry portfolios show evidence of cointegrated behaviors. Analysis shows that 2 cointegration relationships may exist for Variance premium, Credit, Liquidity, hence Variance premium, Liquidity and Credit share the same common stochastic trend. Using our daily data sample, in a pricing discovery sense, volatility premium always leads both credit default swap (CDS) spreads and bond market liquidity. Credit spread sometimes leads bond liquidity, however liquidity never leads either credit spreads or variance premium. As documented in previous studies, credit spread level, as a proxy for credit quality, strengthens the model explanatory power for the credit spread equation.

Pair-trading strategies between CDS portfolio and VIX futures portfolio are significantly profitable with Sharpe ratios in excess of 5 across all credit sorted and industry CDS portfolios. This empirical evidence makes the case for the existence of cointegrated behavior between CDS spread and variance premium more robust. Profitability of the pair-trading strategy is volatility regime dependent: strategy is more profitable in low-volatility regimes than in high-volatility regimes.

Contribution to cross-asset price discovery literature:

- Whereas previous studies have investigated pricing discovery and possible spillovers between credit spreads derived from equity using structural models, CDS, options and bond market, to the best of our knowledge, this is the first study linking an investable measure of variance premium, corporate credit spreads and a cash bond liquidity gauge in a VECM framework.

- We show the leading role of implied volatility market over the CDS market and aggregate cash bond market liquidity, which is consistent with previous studies linking stock returns, corporate bond spreads and CDS spreads. Bond market liquidity fluctuations are a reaction to equity volatility shocks and not themselves the generating source of market disturbance.

- These stylized facts have important implications both for market participants and policymakers. The former are interested in identifying market-leading information. The latter, focused on financial market stability, should benefit from a precise understanding of market linkages since identifying which market drives volatility spillovers is key to adequate response to financial crises.

To illustrate the practical workings of the strategy, 3 represents the second decile of credit sorted CDS portfolio over VIX constant maturity future during the calendar year 2012. On 2 February 2012, a purchase CDS –long protection- sell VIX signal with a beta of 0.0033 is triggered. The position remains open until 8 February, when an exit signal is triggered and the position is unwound at a profit of 11bp. Over calendar year 2012, a total of 8 signals are generated, of which 3 are long CDS short VIX and 3 are long VIX short CDS.

[1] Hasbrouq (1995) attributes a greater share of the price discovery to the market which contributes most to its variance. Gonzalo-Granger (1995) decomposes the permanent component and attributes the leading role to the market that adjusts least to the price movements in other markets. According to Yan and Zivot (2010), methods can be seen as complementary.

Bibliography & References:

Bakshi G, Kapadia N (2003). “Delta-hedged gains and the negative market volatility premium”, Review of Financial Studies, 16(2), pp 527-566

Bakshi G, Kapadia N, Madan D (2003). “Stock Return Characteristics, Skew Laws, and Differential Pricing of Individual Equity Options”, Review of Financial Studies 16(1), pp 101-143.

Brooks J, Palhares D, Richardson S. Style Investing in fixed income”, Journal of Portfolio Management 2018, 44 (4) 127-139

Eraker B, Wu Y (2014). “Explaining the negative returns to VIX Futures and ETNs: an Equilibrium approach”.Working paper, available at http://ssrn.com/abstract=2340070

Figuerola-Ferretti I, Paraskevopoulos I (2011). “pairing credit risk with market risk” Working paper o2 Universidad Carlos III d Madrid. 2011

Forte S, Pena (2009): “Credit spreads: An empirical analysis on the informational content of stocks,bonds, and CDS”, Journal of Banking

Gatev EG, Goetzman W, Rouwenhorst KG, (2006). “Pairs trading: performance of a relative value arbitrage rule”, Review of Financial Studies v 19 n 3 2006

Johnson TL (2017). “Risk premia and the VIX term structure”, Journal of Financial and Quantitative Analysis 2017.

Yan B, Zivot E (2010) : A structural Analysis of price discovery measures, Journal of Financial Markets, 2010

Wang H, Zhou H, Zhou Y (2013): “credit default swap spreads and variance risk premia”, Journal of banking and finance Oct 2013