Family business growth: an integrated perspective

Société des établissements Bougro (SODEBO) has succeeded in breaking growth records and climbing to the top of the podium, while remaining 100% family-owned and totally independent (no bank financing).

Thanks to innovation, a culture of family spirit, and above all total control of the production chain (zero sub-contracting), the family business (EF) has more than doubled in size. The co-chairmen, Patricia Brochard, Marie-Laurence Gouraud and Bénédicte Mercier, all grew up in the company, working alongside their parents, Simone and Joseph Bougro, the founders. Somewhat along the lines of the Mulliez family, the Bougros hope to integrate the growth of the family with that of the company, by encouraging family members (spouses, children, sons-in-law, etc.) to participate in the company's capital and management. The implementation of growth strategies (development of new products and/or markets, internationalisation, diversification, etc.) in family businesses is influenced by certain family objectives and needs. So how do you take a family business to the next level, under optimum conditions?

The growth of a family business requires a dual choice of investment and financing

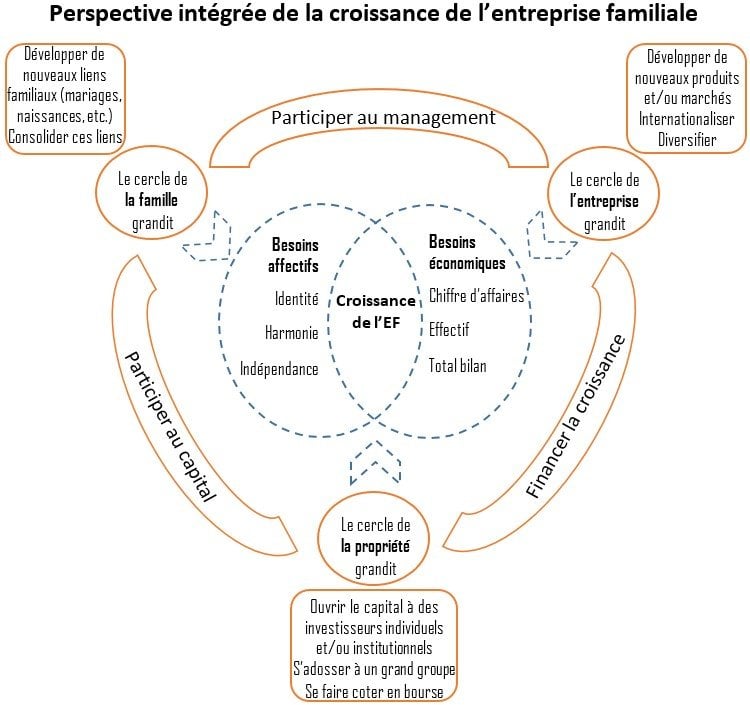

Should the company invest in developing its business through its own resources (organic growth) or by acquiring existing companies or goodwill (external growth)? Should this growth be financed by retained earnings (self-financing), credit from banks and other partners (debt), new family shareholdings (family equity), or by opening up the capital (external equity)? The specific nature of this dual choice lies in the economic, financial, socio-psychological and governance issues involved. In terms of investment, the creation of new units instead of developing the old original unit could, for example, make it possible to limit conflicts between potential successors, or between different generations in the case of a multi-generational family business. It is not uncommon these days for family businesses to be made up of up to four generations. In such cases, the needs of each generation must be taken into account. On the other hand, the purchase of small family units with no successors, or which are looking for a group to back them up, can provide an opportunity for geographical coverage. However, in order to avoid damaging the group's socio-emotional wealth, they should be well established locally, have an excellent reputation and their managers should be committed to supporting the group in order to retain the business. As far as financing is concerned, although it is true that retained earnings can strengthen the independence of the family business, it is above all the choice between opening up or not opening up the capital that needs to be clarified. While opening up capital is a way of sharing risks with an outside investor, benefiting from its networks and advice, and strengthening equity capital, it can also mean family disengagement, a loss of autonomy and independence, a risk of exposure of family affairs, power sharing, and a risk of losing family control. Opening up the capital can therefore be a solution when the family's equity is insufficient, and enables a balanced family estate to be maintained as part of an external diversification strategy.

New family ties such as those resulting from marriages and births [...] can be used to measure the growth of social capital [...] a real asset for the family business.

The growth of the Family Business must be accompanied by a sound risk diversification strategy

We need to distinguish between internal diversification (developing several activities within the family business) and external diversification (maintaining a certain proportion of the family's assets outside the family business). On the one hand, the family business may be tempted at an early stage to want to develop new activities or conquer new markets, to the detriment of consolidating its core activities and markets, and thus run the risk of disintegration. It is important to realise that a sectoral retreat does not preclude geographic expansion. On the other hand, the desire for growth can lead to the family business retaining too large a share of its assets. It may force the family to increase its shareholding as the business grows, by contributing new family funds, or to excessively limit the distribution of dividends. This can be a formidable trap for family shareholders. In this respect, the balance of family assets is crucial to avoid jeopardising the future of heirs, and to limit the frustration of passive members and unjustified withdrawals by active members.

The Family Business must ensure the growth of both the business and the family.

Because the strengths and weaknesses of family businesses lie in both their economic and social capital, they should not attempt to measure their performance using exclusively quantitative criteria. Changes in sales, the number of employees or the balance sheet total, which are very often used in financial analyses and forecasts, do not take into account the family circle, an essential component of the family business. Much more qualitative criteria need to be incorporated. New family ties, such as those resulting from marriages and births, the increase in the family group's ability to mobilise networks, and above all the quality of these relationships, can thus make it possible to measure the growth in social capital, which can constitute a real asset for the family business. It should be noted, however, that as the family grows, conflicts may arise between potential successors, and also, that some parents in advanced age may adopt an attitude favourable to the status quo and paralyse the growth of the business.

Family Business growth must not destroy more than it creates

The value of a family business is not just financial (satisfying economic needs), it is also socio-emotional (satisfying emotional needs). Caution must therefore be exercised to avoid "destructive creation". Indeed, maximising the financial value of the family business can often involve adopting managerial strategies and practices that are far removed from the family style and fail to take account of the emotional needs of family members. The organisational changes associated with the implementation of these growth strategies can certainly limit the altruistic and nepotistic behaviour inherent in the family character, but can also undermine the flexibility, solidity, resilience and ability to adopt a long-term vision that are the strengths of the family business and its management style. It is also important to pay particular attention to the distance, not only in terms of hierarchy, but also in terms of vision and values, which can increase between family controllers and non-family agents of the business, generating information asymmetry and agency costs.

![[#dataviz] Santé connectée et IA : quelles tendances pour 2026 ?](/sites/default/files/styles/actu_850_480/public/2026-03/2026-03-header-dataviz-vox-sante-connectee.jpg?itok=DO57eudN)